What Do You Need to Know About Payment Processing?

The essential guide for beginners

Building your e-commerce store is exciting, but working hard and offering products or services you’ve created without having a payment process is like doing nothing. So you need to understand how the payment process of e-commerce works to avoid mistakes or misunderstandings.

How would you continue with your business if you don’t get paid? Therefore, being knowledgeable about your finances is what is going to keep you alive. Understanding the whole process of credit card charges is crucial to staying on top of your earnings.

- This guide will give you a basic knowledge of the payment process. However, it is essential to read all the regulations and stay aware of payment processor fees to avoid discrepancies in your earnings. Also, all payment processors have fees and special rules, which you can locate on their sites. The costs will apply to your sales depending on the payment processor you use or are offered to use.

What Do You Need to Know First?

You need to know some essential elements of the online payment process. These fundamental elements are necessary to each other and the whole process itself. If one of these elements is missing, the entire procedure will not work.

Merchant Account

A merchant account is a bank account to transfer payments. Once the customer pays their transaction, it needs to be authorized and recognized. Then, the payment goes from the customer’s credit or debit company to the merchant’s bank account. After a few days, the amount is transferred to the business bank account.

For those with a physical store (brick-and-mortar), you can choose between a dedicated account (the payments are transferred to your account within a couple of days) or an aggregated account (like Stripe offer, which is a payment processing account without the need of merchant account and payment gateway).

Acquirer Banks

The acquiring bank provides merchant accounts to businesses. In addition, they have the authority to process credit card and debit card payments on behalf of merchants (vendors). Acquiring banks follow stringent PCI-DSS mandate regulations. Some examples include institutions like HSBC, Bank of America, and Scotiabank.

Issuing Banks

Issuing banks refer to the customer banks. They have the role of restricting or denying card applications based on the consumer’s credit. The issuing bank must ensure the customers has the resources to cover the total of each transaction. The primary purpose of the issuing bank is to provide small, unsecured loans to cardholders in exchange for monthly fees. Some examples are Chase, Wells Fargo, Charles Schwab, and Bank of America.

Payment Processor

A payment processor is the “middleman” between the merchant and the financial institution. The primary purpose is to manage credit card transactions. The payment processor transmits the information between the customer’s card bank to the commerces bank. It facilitates the transfer of funds. In addition, payment processors enable PCI-compliant assistance, issuing credit limits, and charging equipment, among many other services. Examples of payment processors include FIS, PayPal, and Stripe.

Payment gateway

The payment gateway is the system or tool that reads and transfers payment information from the customer’s bank to the merchant account. The primary purpose of the payment gateway is to capture the data to ensure the customer has the necessary funds to pay for the goods. In addition, it connects the online store with the payment processor. In other words, it retrieves the cardholder information and sends it to the acquirer bank through the gateway. Examples are PayPal, Stripe, Square, Secure Pay, Worldpay, Authorize.net, 2Checkout.com, and Braintree.

Tokenization

Tokenization refers to the method of protecting the customer’s payment information. The process consists of substituting sensitive data (like credit card numbers) into non-sensitive data called tokens. For this, the private data needs to be under the tokenization method. The payment gateway substitutes the personal data for a token; this way, the information is secure if there is a breach. For example, instead of requesting a charge to Visa number 123-45-678, the request is something like this, “please request payment to token 124578.”

SSL certificate

An SSL certificate is a digital certificate that identifies a site and enables an encrypted connection. The purpose of SSL is to keep internet connections secure and prevent hackers or criminals from reading and changing information. Getting one to run a secured site is necessary, and they are very inexpensive. Implementing security on your site help with customers’ trust and, as such, in conversions.

PCI compliance

PCI Compliance refers to the regulations merchants must follow to accept payments. Several levels correlate to different layers of security for payment processing. For example, merchant accounts can require different levels of compliance to accept payments (some allow using an SSL certificate alone while charging a monthly fee for non-compliance). There are two processes; the first one refers to the payment being outside your site, like, for example, PayPal Standard; the process is PCI compliance because the site never handles sensitive information. On the contrary, if the process is handled through the site, an integration must affect how PCI is handled.

What are the most typical online payment methods?

There are various forms of online payments. There are more than $1 billion in e-commerce sales in the US daily. Imagine the number of transactions and money there is involved in each transaction.

Visa and Mastercard

The leaders as payment methods by US buyers. They are in 95% of the top 500 e-commerce, according to Statista. American Express is following the steps of these two titans with an 89%.

Alternative Payments

The second-largest methods buyers use are PayPal (widely used worldwide), Amazon Payment card, Google Pay, and Apple Pay. Buyers also extensively use other payment processors that allow people to pay in installments: Affirm, Afterpay, Klarna, and Sezzle.

Direct Debit

Under these methods fall the debit card and e-check

Direct Payment

Refers to the person-to-person payment done with cash, but this method is less recurrent.

Digital Currency

This type of method, known as cryptocurrency, is taking more acceptance among vendors. Large companies, as well as countries, are using this type of method. Among the most famous are Bitcoin and Ethereum.

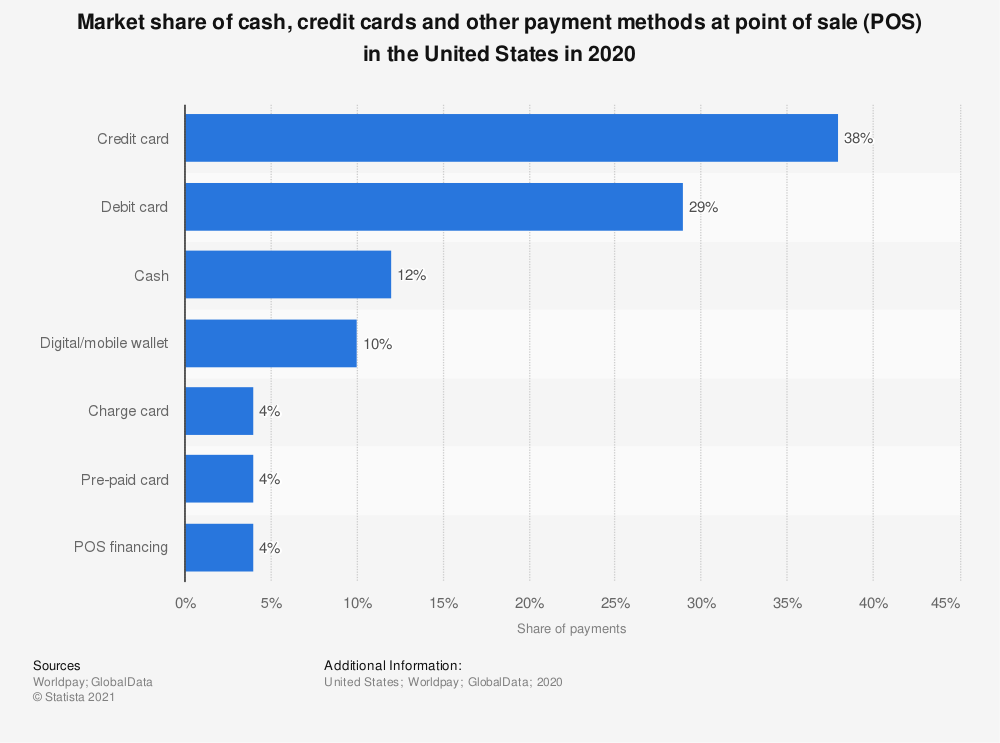

You can give your customers a few other options for paying online during the checkout process, such as ACH and invoicing. However, as you can see from the chart below, credit cards, alternative payments, and direct debit are the ones most people prefer.

How to use some payment methods?

Each payment method has its process as well as fees. Therefore, the user must know the costs before committing to specific payment methods.

Credit cards

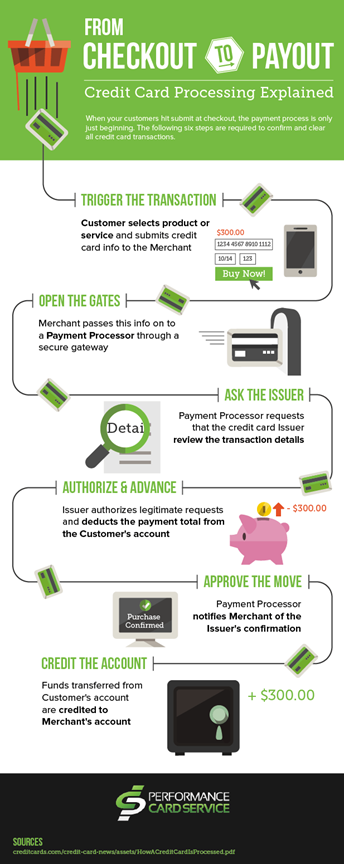

As mentioned before, credit cards are widely accepted throughout most e-commerce and physical stores. So, providing a credit card payment method is a plus for your business. Now, what is the process of using credit cards? Here it is:

- The customer enters all credit card personal information on your site.

- The payment gateway receives the details and the amount to be charged. The payment gateway has the job of rejecting or approving the transaction. Then the information is passed to the e-commerce site with the good or bad news. If it is rejected, the transaction stops there. If it is accepted, then,

- The Payment is accepted, and the process of checking out is completed.

Check this in-detail credit card charge process from https://pdcflow.com.

PayPal

PayPal is widely used worldwide as well as greatly accepted by customers. Depending on the type that best fits your business, it has different programs for merchants. You can learn more about the different types of accounts in the Jilt. PayPal can increase your sales due to its recognition in many countries and the high acceptance of customers. The good thing about PayPal is that it can accept credit cards and act as a digital wallet by transferring money from one user to another.

eChecks

An eCheck is the digital version of a regular paper check. When using an e-check, the money is electronically withdrawn from the buyer’s account into an ACH (Automated Clearing House) account, then deposited into a merchant’s account. The ACH has the authority to withdraw payments directly from the payer’s account. Still, the payer must authorize the payment through a contract, terms and conditions from the site, or voice recording.

Cryptocurrency

Among the most famous cryptocurrency is Bitcoin. Even though there is still some convincing to do, cryptocurrency is taking place in payment methods. To purchase something using cryptocurrency, you need to have a crypto debit card. Once you have your cryptocurrency on the card is a matter of purchasing wherever you can use it. In most instances, you can buy houses, cars, boats, and other expensive goods! The retailer will not receive cryptocurrency as Payment but flat money. Crypto can be exchanged into fiat money because it partners with Mastercard and Visa to ensure flawless processes.

What is the difference between charge and authorized?

The payment gateway permits you to collect the funds in two ways: through charge or authorization. A charge is when the payment gateway processes the funds immediately from the customer’s account or issuing bank. Authorize, on the other hand, requests if the customer has the funds to cover the expenses. Once approved, the funds are captured and transferred later in a few days.

How to Avoid Fraud on online payment?

Online payment is the weakest point of your site if you don’t take the necessary measures to protect your business. You need to comply with several regulations, but you also require other methods to safeguard critical information. Here are some examples that will help you add a layer of protection to your store or site.

Encryption and Tokenization

Encryption

Encrypt is adding a layer of security by changing the information into a code or encoding. The good thing about encoding information is that you need a key to decode the data. Of course, the information can be obtained through hackers or thieves, but it will be tough if they don’t possess the key to read the information.

Tokenization

Tokenization refers to the method of protecting the customer’s payment information. The process consists of substituting sensitive data (like credit card numbers) into non-sensitive data called tokens. For this, the private data needs to be under the tokenization method. The payment gateway substitutes the personal data for a token; this way, the information is secure if there is a breach. For example, instead of requesting a charge to Visa number 123-45-678, the request is something like this, “please request payment to token 124578.”

Other Types of Anti-Fraud Tools

Address Verification Service (AVS)

The address verification service aims to match the address on-site (usually for shipping) and the card’s bank hold address. If the addresses don’t match, the charges will not proceed.

CVV

The card verification value or CVV is to verify the 3- or 4-digit code necessary to ensure the card’s owner is holding the card. Most fraudulent charges are done by those not carrying the card.

Use 3D Secure 2.0

Implementing 3-D Secure (3DS) provides another level of fraud authentication by asking customers to enter a predetermined security code. Fraudsters would not know the security code, so the transaction is stopped without the code.

Another way to protect your business is to verify the list published by Experian. The list is based on zip codes primarily associated with fraudulent transactions.

Recognizing Potential Fraud

Certain types of transactions are more susceptible than others, such as online payments. Here are examples of trades you should be aware of to avoid cyber-shopping fraud.

International orders – they are three times more frequent than thought. Unusually large orders – if you receive a substantial order, it may be a fraud.

Order risk – if you believe you have an order that looks senseless or fishy, pay attention to your intuition because it can cost you further.

Check the zip codes- be aware of those areas with high cyber fraud.

Download a list of shipping zip codes.

Download a list of billing zip codes.

Check this information provided by the US FBI here.

How to Avoid Chargebacks?

A chargeback is a protection the consumer has to request their money back after a purchase. In most instances, the charges are fraudulent, or the purchases are not to the customer’s standards. Each card has a maximum fee which can go from $20 up to $100.

- Use Address Verification Service (AVS)

- Require card security codes.

- Use 3D Secure 2.0__, an industry authentication protocol with the default mechanism for strong (two-factor) authentication.

- Enroll in-network automated response.

- Network automated__ is a service provided by Visa and Mastercard to help customers recognize charges that, for one reason or another, are not recognized by them, even though they are the initiators. Visa holders use Order Insight, where real-time merchant data is provided to corroborate charges. Mastercard has a service called Consumer Clarity, which is much the same as Visa.

- Provide Excellent Customer Service

- Offering excellent customer service is a great way to handle customers before, during, and after a service, lowering the number of chargebacks.

- Give information on requesting a refund or dealing with a wrong order. Informing the customers about specific processes will keep communication open.

- Follow up with complaints, especially if they are done through social media.

- Review the return and cancellation policies. Make them more friendly and accessible.

- Review the customer journey during all the phases of purchasing, even after shipping.

- Audit customer service experience. Identify the weaknesses of the operation.

- Be aware of product descriptions.

- All product descriptions should have a length of about 400 words. It must be precise, concise, and include an authentic product features and conditions narrative.

- The description must include photos.

- The description should include a video.

- A new vendor must be aware of the signs.

- Always keep a record of the shipping information, the product, and the tracking number before shipping as part of the evidence against chargeback fraud.

- Take a video of the return package before opening it.

- Keep a record of ID numbers or any specific identifier.

- Send the correct size based on the measurements selected by the customer.

- Provide a size chart next to all products where measurements are needed and explain if the merchandise has Asian, European, or Western sizes (they are all different).

- If the merchandise passes a certain amount, for example, $250.00, you can add a signature to the delivery request.

- Purchases in volume but different sizes, for example, 20 pairs of shoes, all in various sizes.

- Large ticket items (luxury or expensive goods) are favorites of fraud purchases.

- Purchases paid with different cards and shipped to the same address or vice versa, multiple purchases on one card and shipped to separate addresses.

Credit Card Information You Should Be Aware of

Press on each one!

There are many other payment processors. It would be best to verify which is the best for your business with the lowest fees. Remember, it is your business and your proceeds, so protect them!

Blogs you should read to learn more about this topic

- Merchant Services Fees Explained

- Understanding credit card merchant fees: What are you paying for, and whom are you paying?

- Understanding Credit Card Processing Fees and Chargebacks

- Credit Card Processing Fees and Costs